|

|

s: flow supply h: flow demand p: price AI: actual stocks DI: desired stocks r: interest rate pe: expected price |

|

pe = f(p,...) |

|

AmbienteDiritto.it - Rivista giuridica - Electronic Law Review - Copyright © AmbienteDiritto.it

Testata registrata presso il Tribunale di Patti Reg. n. 197 del 19/07/2006

An applicable update on the world oil market

Ferdinand E. Banks*

Abstract

This paper extends the work on peak oil that has been published in my

earlier papers, and also in my forthcoming energy economics textbook (2007). I

am particularly interested in correcting some of the mistakes that have and will

be made about the future supply of oil. One point that deserves to be emphasized

is that oil is already scarce in relation to the future demand for this

commodity. Furthermore, this situation has finally been recognized by most OPEC

countries, which explains why they are in no hurry to expand their capacity.

Instead, many of their investments are being directed into the processing of

crude oil into oil products, and once these products are available some of them

could be used with the ample supplies of natural gas in the Middle East as

inputs for greatly increasing the production of petrochemicals. I am also

positive about ethanol, bio-diesel and hydrogen, despite the criticism they have

received of late. It is probably true that these items should not be produced in

the quantities apparently suggested by the present governor of California and

the president of the United States, but a certain amount are necessary as a kind

of insurance. There are many unpleasant macroeconomic events to which North

America and Europe could be subjected at the present time, and the belief here

is that these could be unleashed by a sharp and sustained oil price escalation

due to the opening of a gap between oil supply and demand.

Key words: Peak oil, game theory, tar sands and heavy oil, hedge funds.

Applicable how? Applicable in the sense that one of the cardinal rules of

physics has traditionally been that the introduction of new concepts was not

more important than abandoning some of the mistaken notions that often find

their way into widespread circulation. This is why I offer the present update,

instead of upgrading one of my earlier contributions, or for that matter

reworking a portion of the chapters on oil in my forthcoming energy economics

textbook (2007). Those materials are not yesterday’s news, but things move fast

in the great world of oil, and unfortunately new events do not always receive

what I regard as an appropriate interpretation.

For instance, in the section below titled ‘The Logic of Peak Oil’, I am

essentially inquiring how a new author, Mr Duncan Clarke (2007), could possibly

come to the conclusion that the flaw in the peak oil argument is that it ignores

the basic rules of economic theory, which to his way of thinking stipulates that

when the price of something goes up, it is always the case that either supply

increases or demand falls or both. When a student of economics makes this claim

about a non-renewable resource, I usually call it a misunderstanding.

Originating with someone who enjoys a background in economics as well as three

decades of rubbing elbows with oil company executives and experts, it shows a

disturbing lack of perception.

As Professor Julie Urban pointed out (2006), economists are wrong by continuing

to believe that price increases can locate resources that do not exist in the

quantities required. As for a fall in the demand for oil, this is an issue that

might have some traumatic macroeconomic overtones, as will be noted later in

this introductory section. A slender bundle of pseudo-scientific hand-me-downs

has also been served up by two authors under the sponsorship of a Washington DC

‘think tank’, the Cato Institute, whose energy and climate delusions are

financed to a certain extent by the largest oil company in the world, ExxonMobil.

The gentlemen in question are not in the oil business, nor are they economists,

but are respectively professors of government and public affairs, which means

where this topic is concerned that they have little more to provide than rappers

or do-ah choristers.

It has now become clear to a large number of concerned observers that October,

1973, was a turning point in modern economic history. Aside from the near panic

that accompanied the first oil price escalation (or ‘shock’ as it is

sometimes called), my most vivid recollection of that dramatic period was the

general failure by economists and politicians to comprehend the character and

significance of OPEC, and what the logical and legitimate ambitions of certain

key OPEC countries could or would eventually mean for the politics, philosophy

and economics of virtually every country in the world, regardless of their

access to oil or other energy resources.

Somewhat earlier, Enrico Mattei had coined the phrase “the Seven Sisters” to

describe the petroleum world’s movers and shakers. The Seven have now morphed

into Four – ExxonMobile and Chevron of the US, and Europe’s British Petroleum

(BP) and Royal Dutch Shell. According to a recent article in the Financial

Times (March 12, 2007), there is a new Seven that deserves at least a

modicum of attention: Saudi Aramco, Russia’s Gazprom, CNPC of China, NIOC of

Iran, Venezuela’s PDVSA, Brazil’s Petrobras and Petronas of Malaysia. These are

important enterprises, and CNPC and Petronas are particularly aggressive, but

with the exception of Aramco and Gazprom, not yet in the ‘class’ with the above

four. For instance, Iran has 11% of world oil reserves, and after Russia is the

most important natural gas nation, but unfortunately there is some evidence that

it will not be able to make the kind of contribution to the global energy supply

that will be necessary to keep the oil wolf away from the door.

According to Roger Stern (2006), Iran could stop exporting oil as early as 2014

– presumably because of a greatly increased demand for transportation fuels in

that country and adjacent regions. This does not sound completely right to me,

even if it is possible to accept the suggestion that Iranian export capacity may

develop in a manner that will be well under that predicted by e.g. the

International Energy Agency (IEA). Professor A.F.Alhajii, for instance, contends

that Iran can increase production to 4.8 mb/d, and maintain it at that level for

than 20 years if they desire (2007). Regardless of Iran’s capabilities however,

one thing deserves emphasis: if Iran’s contribution to global supplies turns out

to be less than desired, it is not because of any technical or managerial

shortcomings on the part of Iranians that would be ameliorated by inviting

foreigners to explore for and extract oil and gas in their country.

According to the IEA, ninety percent of new oil supplies in the next 40 years

will come from developing countries. Ordinarily this could be regarded as a

cheerful piece of news, however I am so accustomed to flawed IEA prognoses that

I am unable to take it as a given. For example, it appears that Saudi Arabia (with

22% of world reserves) has convinced that organization and a few others that

they will boost production capacity to 15 mb/d, or thereabouts, in the not too

distant future. This will almost certainly not happen, however if it did it

would not make the forecasts of the IEA and the United States Department of

Energy (USDOE) more palatable. For that Saudi production must eventually rise to

20 mb/d of the predicted 121 mb/d that has been forecast by those two

organizations for 2030, and this is completely out of the question. In the

executive suites of Big Oil, a sustainable output of 121 mb/d at any time in the

future is generally regarded as being without any economic or geological

feasibility, regardless of what the directors of the ‘Big Four’ say when the TV

cameras are turned in their direction.

I utilize a small portion of my new textbook to examine the above predictions,

and also to argue that more attention should be paid the macroeconomic and

political situations that could unfold in the event of explosive price rises

that could accompany or even precede a peaking of the world oil output. The

price of oil determines the price of most energy resources, and definitely the

other fossil fuels – gas and coal. An abrupt energy price escalation could

therefore have a sharp impact on productivity, which in turn would have a

negative effect on employment and the remuneration of employees. It might also

lead to a decision by large numbers of voters in the energy importing world that

military action launched to obtain energy supplies is preferable to even a mild

decline in their living standards that has the possibility of being irreversible.

Something else that it could mean is an additional resort to coal that would

cancel out all the fine theories and intentions expressed in the Kyoto Protocol

and its spinoffs. The USDOE has estimated that electricity demand in the US will

increase by 45% between now and 2030. Coal usage is scheduled to grow from 51%

to 57% because of its availability and price, but a sustained escalation of the

oil price would be certain to boost the price of gas, which according to a study

by Sanford C. Bernstein & Co., already costs 30% more than coal on the US

electricity generation front, even if a very high price for the suppression of

carbon emissions is assumed. Coal might then attain more than 60% of the energy

mix, with ‘clean coal’ playing only a minor role. As for the kind of

coal-burning plant called FutureGen, which would trap carbon dioxide before it

reaches the atmosphere and bury it below ground, if it corresponds to the

efforts in that direction by the large Swedish firm Vattenfall, it is strictly a

play for the gallery.

The principal theme in what follows has to do with the return of OPEC to the oil

market driver’s seat, the genuine shortage of energy materials in terms of the

amounts that are desired, and the growing ability of formerly monolithic state

oil companies to alter the competitive landscape in oil, oil products, and

petrochemicals.

Game Theory and unconventional oil

This exposition is essentially the final lecture that I gave in the Spring

course on oil and gas economics at the Asian Institute of Technology (Bangkok).

For years, in one form or another, colleagues and conference acquaintances have

tried to convince me of the mistakes being made by oil producers in e.g. OPEC in

regard to their export policies, and in particular a hypothesis was passed

around seminar rooms and conference locales that Gulf producers should recognize

that a long stretch of oil at $25/b is preferable to the discomfort that would

eventually be imposed on them if they immediately increased the price of their

oil to $30/b or higher. One of the persons taking this position was a former

Saudi oil minister and OPEC chief, Ahmed Yamani, who insisted that there were

still stones in plentiful supply when the Stone Age came to an end. Exactly what

this charming reality had to do with oil is uncertain, because given the

realities of global population growth, oil is going to be more valuable than

ever in a future where huge quantities of transportation fuels and

petrochemicals are going to be essential. With this in mind, the Saudi oil

minister, Mr Ali Naimi, has said that his country would increasingly use its

natural gas and growing petrochemical output to form clusters of industries,

which implies modifying – and perhaps to a considerable extent – its traditional

roll as an exporter of crude oil..

Before continuing, it might be a good idea to introduce the word ‘game’ into the

present discussion. In the Hollywood travesty of the book A Beautiful Mind

(1997), game theory was presented as an authentic scientific pursuit rather than

the description applied to it by Professor Erich Röpke, which was “Viennese

coffee-house gossip”. Actually it is a combination of both, in the ratio of

about one-in-five, and this is despite its prominence in esteemed (though

largely unread) journals of quantitative economics, as well as the widely

circulated opinion that “it is impossible to understand modern economic thought

without a grounding in game theory.” On the whole game theory has failed to

deliver, although it was introduced into the modern economics literature by a

man often credited with the best brain of the 20th century, John von Neumann.

At the same time it can be admitted that there are certain things that game

theory has spotlighted that are of considerable value in analyses of the present

type. People sometimes act irrationally but are also capable of thinking

strategically, and skilled players more often than not consider all possible

outcomes, and constantly attempt to evaluate the meaning and possible evolution

of alternative payoffs. What John Nash – the proud owner of A Beautiful Mind

– ostensibly did was to carefully formulate a theory in which equilibrium means

that each player cannot improve his or her position by making an alternative

choice. What actually happened was that Nash took a few minutes to recast a

notion that had been published at least a hundred years earlier by Antoine

Cournot, and for which he was eventually awarded a Nobel Prize in economics.

In my lectures I have used game theoretical concepts to discuss unconventional

oil, and also oil found in unfamiliar locales, such as the Caspian region. The

basic issue here is not an ‘equilibrium’, but the astounding quantity of

misinformation and misunderstandings put into circulation by ‘players’ with

interests in these locales, as well as their official and unofficial

propagandists. For instance, one of the best introductions to oil from Canadian

tar sands, and heavy oil (from Venezuela) can be found a recent OPEC Bulletin

(March, 2007). It happens though that oil from these two sources is a growing

competitor of conventional oil (from e.g. OPEC countries), and so a question

must be asked about the enthusiasm shown unconventional oil by an OPEC

publication. The reason quite simply is to give the impression that despite the

warnings circulated by persons like myself, both governments (and perhaps

consumers) in the oil importing countries should come to accept that there will

be plenty of oil available in the distant as well as the near future, and very

likely at prices that they find reasonable.

Saudi Arabia enjoys a special position where conventional oil resources and

production are concerned, but now we often hear that Saudi reserves may not be

in the same class as those found in Northern Alberta (Canada). Furthermore, the

latter might be overshadowed by the resources of the Orinoco Oil Belt in

Venezuela: the OPEC discussion cites estimates of Petroleos de Venezuelas, which

puts the present estimated content of the Belt at 235 billion barrels of heavy

crude, which with likely additions should eventually be sufficient to cause it

to be labelled the largest petroleum reserve in existence.

The question must then be put as to the cost of exploiting tar sands and heavy

oil. Forty dollars per barrel is the highest figure that I have ever seen, which

would suggest that with an oil price unlikely to fall below fifty dollars per

barrel ($50/b), an oil shortage during the present century is a physical

impossibility, and the Schwartzenegger/California type of initiative featuring

ethanol and/or hydrogen is unnecessary. Actually, as an ‘insurance’ against oil

price spikes, it is essential, although there is no need to launch an

undertaking of Manhattan Project size until the technology for these departures

is further developed.

Furthermore, according to the Toronto Star (Wednesday, 25 April, 2007),

the supplies of easily exploitable Canadian oil have almost run out, and so

conventional oil royalties are only one-third of those obtained two years ago.

Oil sands royalties are also declining, apparently because of a lower rate of

growth of tar-sand output: perhaps only 3 mb/d in 2020 as compared to 1 mb/d at

present. If this figure is anywhere near the truth, tar sands are not going to

save the day for North American consumers, regardless of the huge reserve

figures that we constantly hear so much about. For example, when Shell Oil

states that they might have access to an impressive slice of the 2 trillion

barrels of oil reserves that they believe could eventually be located in Canada,

they are sending a message to present and potential investors in their shares

that great things are ahead, despite any disappointments or negative press that

they might have been exposed to over the past few years.

As for heavy-oil in Venezuela, Major Chavez obviously intends to make sure that

if he has the option, its output will be such that it does not spoil the market.

Although it may appear that he has even less respect for Adam Smith’s “invisible

hand” than his famous friend in Cuba, the simple fact of the matter is that like

Mr Smith and his disciples in the executive suites of Big Oil, he prefers more

money to less. The last foreign controlled oil field in his country – in the

Orinoco Belt – has been nominally nationalised, which means that the Venezuelan

government will assume majority control of four heavy oil projects, and thus

reduce the stakes of ConocoPhillips, Chevron, Exxon Mobil, Total, BP and Statoil

by a few billions of dollars, but as far as I can tell there will still be a

foreign presence in the Venezuelan energy industry.

Given that Canada and Venezuela are the flagships of tar-sand and heavy oil

hopes and dreams, the future of non-conventional resources may not be as bright

as many persons in the main oil importing countries have come to believe, in

that these resources will not be available in the near future in sufficient

amounts to relieve some of the demand pressure on conventional resources. Of

course there is still shale oil, in which the US appears to be the world leader,

however in my opinion the touting of shale oil is perhaps the biggest scam yet.

Now we see what game theory is largely about outside the seminar room and

learned journals. Not “beautiful mind games” that provides academics and policy

makers with an important new analytical means to study human behaviour, but to

an embarrassing extent a refined and overpraised outlet for the presentation of

untruths and misunderstandings.

The logic of peak oil

Oil has been discovered in many countries, and in a substantial majority of

those countries its output has already peaked or levelled off, resulting in a

plateau instead of a distinct summit. Here I am talking about both huge deposits

– or ‘elephants’ as they are sometimes called – and back-yard deposits of the

kind that once were said to be common in California. The question then becomes

how oil production could peak in large regions like the US and North Sea, as

well as enormous deposits like Burgan (in Kuwait) and Cantarell (in the Gulf of

Mexico) – the second and third largest deposits in the world – and not peak

globally, by which I do not mean about the middle of the present century or

later. The thing to note here is that oil production peaked in the two regions

mentioned above about 40 years after discoveries peaked, and globally the

discovery of conventional oil peaked in l965. As for Burgan and Cantarell, they

have not only peaked but Cantarell is apparently in rapid decline.

One often exploited origin of non-peak arguments turns on assuming that

unconventional oil of the kind discussed in the previous section is in reality

conventional. On the basis of the discussion in that section however, this would

not change very much. Unconventional oil at the present time is about

reserves and not production! The presence of hundreds of billions or even

trillions of barrels of reserves of unconventional oil in Canada and South

America may not have a sizable effect on the date of the global peaking of

production, even though a great deal of unconventional oil is going to be

produced in the years to come, and under certain circumstances could push the

peaking of conventional oil into the future by a few years. It is not peaking

but the effect of actual or putative peaking on the price of oil that is the

main issue here.

For what it is worth, drawing on the contributions of others, I estimate that a

peak for all oil (i.e. conventional and unconventional) will take place between

2015 and 2020. Most independent observers and energy professionals with a deep

interest in oil would probably be able to go along with this, although the

estimated time to the peak appears – on the average – to decrease every year,

and there are even claims that the peak for conventional oil has already taken

place. On the other hand, Shell sees a peak coming after 2025, while the United

States Energy Information Administration (USEIA) and United States Department of

Energy (USDOE) think that a peaking can be delayed until after 2030. The

important consultancy Cambridge Energy Research Associates (CERA) thinks that

there will be an undulating peak instead of a distinct peak. In my course at the

Asian Institute of Technology I described this prediction as a touch looney,

although it might make sense in an elementary economics class at some storefront

university in Boston or New York.

ExxonMobil sees no peak at any time, and the often quoted Michael Lynch is also

unable to discern a peak: his clients have been duly informed that they should

find something else to be concerned about than an explosive oil price

escalation. Before the recent price run-up, Doctor Lynch argued that the price

of oil would decline to about $25/b. OPEC also denies the presence of a peak,

but like Big Oil they find it sensible to try to convince the persons and firms

on the buy side of the oil market that any apprehensions they may have about the

future availability of oil are ill-considered. The energy director of the

European Union has called the discussion about peak oil just another theory

among many. He has a similar belief about the obvious failure of electric

deregulation, which leads me to believe that the extent of his knowledge about

these (and probably many other) topics is best not discussed in a public forum.

In my lectures I always deal with this problem in terms of the history of oil in

the US, viewed in the light of a variant of (Albert) Einstein’s equivalence

theorem (which is explained in some detail in my international finance book).

What I do with this subject is to start with the equivalence of the laws of oil

production in the US and elsewhere, and argue that the peaking of oil output in

the US is a microcosm – or was a preview – of global peaking. Once I have the

bottom line, I explore some of the details.

Oil was discovered in Pennsylvania just before the US Civil war, and later was

produced in appreciable amounts in that state and a dozen others. It was the

discoveries in Oklahoma and California, and in particular East Texas that made

the US an oil superpower. Oil discovery peaked in 1930, while in late l970, to

the surprise of oil scholars everywhere, production peaked in the ‘lower 48’.

The oil output story for the entire country (i.e. 50 states) changed however

when the huge Prudhoe field in Alaska came on stream, which meant that the oil

production curve for the US turned up. But even given the magnitude of that

field, production never achieved the l970 level.

What about technology riding to the rescue, as President George W. Bush has

predicted that it will. No country in human history has had the access to

scientific and engineering knowledge that is enjoyed by the United States of

America, but all attempts to reverse the ongoing depletion of oil, whether

onshore or offshore, have been in vain.

As things now stand the US consumption is approaching 22 mb/d of oil, of which

about 60% is imported, according to the important and reliable Oil Depletion

Analysis Centre (ODAC), whose publications and bulletins can be examined via

GOOGLE. Nobody really expects a change for the better in this situation,

although for the time being the depreciation of the US dollar has taken some of

the stress off the US financial system. But in the long run this depreciation

could lead to inflationary pressures that raise US interest rates, which would

exacerbate the present unfavourable development that seems to be taking place in

the housing market. My macroeconomic knowledge is not as up-to-date as I would

like for it to be, but unless I am very mistaken, the housing market could be

the weakest link in the US economy at the present time. But even if the housing

market does not go sour, something will have to give. It cannot be so that the

US can import hundreds of millions of dollars of oil every day of the year, as

well as fight an expensive war, and the welfare of its citizens is not

influenced in a negative manner.

An even more bleak story is available for the UK. The first exploration licences

for North Sea oil were awarded in l964, and oil production peaked at 2.7 million

barrels in l999 (or 2.9 mb/d if natural gas liquids are included). The

interesting thing here is that in l991 there were 100 fields in production,

while in l997 there were 186 offshore fields in production. Moreover, although

in the early years of this century the UK government talked of 300 discoveries

awaiting development, exploration levels in e.g. 2002 were the lowest since 1970

(according to Dan Roberts and Carola Hoyos of the Financial Times).

Several insiders have claimed that oil prices were not high enough to go after

the oil remaining in the UK North Sea, but this situation has not changed to any

great extent as a result of the oil price moving to record levels. Like many

regions in the world, the North Sea no longer contains any easily exploitable

reserves. This should have been obvious when Sir John Browne announced that in

the future BP would concentrate on profitability rather than property.

Optimists are not particularly concerned with the way things have gone in North

America and the North Sea because of the access that they believe the oil

importing nations will soon have to unconventional oil and/or motor fuels, and

they are also enthusiastic about the Caspian region. According to Professor

Maureen Crandall of the US National Defence University, however, most of the

talk about the Caspian is “hype”. I believe this too, however perhaps it does

not make a great deal of difference, because given the macroeconomic growth of

China and India, and perhaps elsewhere in Asia and South America, every

additional barrel of oil is going to be valuable. There is also a great deal of

talk about the relief that will be brought to the global oil market by new

developments in Africa and increased output in Saudi Arabia.

The opinion here is that much of the talk about the increase in output in Saudi

Arabia is self delusion: the government of that country has finally discovered

that the correct development strategy is to minimize the increase in oil

production, taking into consideration certain political constraints, while the

national oil company Saudi Aramco has said that increasing production too fast

could run down reserves faster than the country would like. This can be put

another way. According to Jim Mulva, CEO of ConocoPhillips, the national oil

companies of countries like Saudi Arabia “may have other strategic objectives,

which may limit the speed by which they develop their resources”. It so

happens that the chief other strategic objective is development! The

director of the important consultancy PFC Energy, Robin West, has brilliantly

summed up this situation by saying that “the full impact of the nationalisations

that took place in the l960s and l970s are taking effect now.”

Analysts at PFC have also stated that the scale of increases in output in

Kazakhstan, Angola, Nigeria and Brazil are limited, and that production in these

countries will also peak in the not too distant future. If this turns out to be

the case for Nigeria and Angola, then all of Africa south of the Sahara can soon

be written off where oil is concerned.

Five years ago a theory was offered by the chief oil analyst of a major

financial company that oil prices would drop as low as $18/b by the following

year, and they would stay there. He argued that the only time in the previous 60

years that the oil price was above $17/b was when there was a war involving at

least one OPEC country, or a member facing political difficulties or embargoes.

The possibility that OPEC had or would become more sophisticated in that it

examined global demand and supply trends and possibilities and reacted

accordingly was dismissed. Perhaps one of the reasons for this ‘optimism’ was

that the futures market predicted lower prices the following year, and recently

even the new director of the US Federal Reserve System referred to the futures

market in such a way as to suggest that it had something to offer when it came

to forecasting future oil prices. In point of truth the futures market has been

a very poor predictor of the actual price of oil since the beginning of the

present century, and most of the time in the 20th century. On this

topic I think it best to pay attention to something that Matthew Simmons of

Simmons & Co – a Houston-based investment firm specializing in oil – once said:

“Too many people are looking at OPEC through the rear-view mirror. There’s a

resolve in their eyes never to go back to the days of cheap oil”. Not just in

OPEC’s eyes but in their investment policies, which make it clear that they feel

that it is in their best interests to refrain from bringing too much additional

oil to market. This is a good place to ask one of my favourite questions: would

you if you were in their place?

Accordingly, the optimal development strategy for a country like Saudi Arabia is

to pay more attention to the refining of oil, and the production of

petrochemicals. There are not only enormous economic possibilities here, but

they have finally been understood and are very likely to be exploited. It is for

this reason that I am positive to a rapid but limited increase in the capability

to produce larger quantities of e.g. ethanol and biodiesel, because even if much

larger quantities are not needed, they are a valuable insurance in the event of

a sudden decline in the supply of conventional fuels. Here it should be

remembered that on the basis of some misunderstanding with Iran about a month

ago, the price of oil suddenly spiked by 5 dollars a barrel.

Conclusion: the oil price and the wisdom of bill o’reilly

Bill O’Reilly is an important political and social commentator in the United

States. He is not important to me of course, even if I agree with a certain

amount of what he says.

I have a serious set of issues however with his beliefs about the oil price. To

his way of thinking the increase in and volatility of the oil price is due to

the machinations of speculators in e.g. Las Vegas. Without these “little guys”,

to use his terminology, or “masters of the universe”, as Tom Wolfe called them –

and occasionally they call themselves – we would have no problem obtaining the

oil that we need, and at prices that we would feel comfortable paying.

What Mr O’Reilly is alluding to are hedge funds, which are also mentioned quite

often in the financial press. I say a few things about hedge funds in my finance

book and my lectures, and I was even given a lecture on these establishments by

a hedge fund hustler just before taking up a visiting professorship in Hong

Kong. The truth of hedge funds is similar to the truth of operations like the

Nordic Electricity Exchange (NORDPOOL). Their strength is in the laziness of

their clients. There are approximately 8500 hedge funds in the world, and every

year about l000 either go out of business or are close to shutting their doors.

It also happens to be the case that the yield on a large majority of those

remaining does not come up to the yield on imaginable unmanaged funds of one

type or another, assuming that it was possible to buy these unmanaged assets.

There are superstars in the ranks of hedge fund managers, but mostly they busy

themselves with the likes of the wealthy Mr O’Reilly, and as the Efficient

Market Hypothesis tells us, most of these superstars are brought down to earth

sooner or later, although when that happens they still have their condos in

Aspen or Monte Carlo.

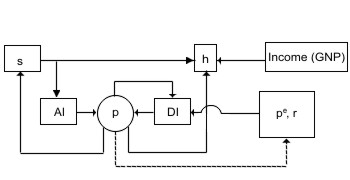

Despite what O’Reilly and others may think, the long run (or trend) oil price is

determined by supply and demand, and the short run price can be described by a

stock-flow model of the type explained at considerable length in my forthcoming

energy economics textbook. Do hedge funds or “little guys in Las Vegas” have

anything to do with this price? Not much, but probably some if we consider the

following diagram.

|

|

s: flow supply h: flow demand p: price AI: actual stocks DI: desired stocks r: interest rate pe: expected price |

|

pe = f(p,...) |

|

Hedge funds and futures markets may influence the expected price, and as a

result the desired stocks (i.e. inventories). If, for example DI > AI because it

is expected that price will increase, then price will increase as an attempt is

made to increase stocks. Readers who are interested in the real world oil market

would do well to examine this diagram and the explanation of its functioning in

my textbook. Nowhere in economics is there a greater discrepancy between fact

and fiction than in the attempt to explain the mechanics of natural resource

markets by esoteric models without the slightest virtue except that the people

who use them find them easier to understand than the real deal.

At the present time I am working on a paper called ‘The architecture of world

oil’, in which some items that could have been included in this paper will be

taken up. Among these will be a more extensive discussion of OPEC, and oil

products and petrochemicals. Hopefully readers will find it interesting and

useful, and it would certainly be nice if other persons – to include students –

would take a more intense interest in oil products and petrochemicals, because

the economics literature on these is very inadequate.

*Asian Institute

of Technology (Bangkok); professor University of Uppsala (Sweden).

References

Alhajii, A.F. (2007). ‘The impact of Iran’s nuclear standoff on world energy

security’.Energy and Environment (Forthcoming).

Banks, Ferdinand E. (2007). The Political Economy of Energy: An Introductory

Textbook. London, New York and Singapore: World Scientific.

______. (2004). ‘Beautiful and not so beautiful minds: an introductory essay on

economic theory and the supply of oil’. The OPEC Review (March).

______. (2001) Global Finance and Financial Markets: A Modern Approach.

London, New York and Singapore: World Scientific.

______. (2000) Energy Economics: A Modern Introduction. Boston and

Dordrecht: Kluwer Academic.

______. (1991) ‘Paper oil, real oil, and the price of oil’. Energy Policy

(July/August).

______. (1987) ‘The reserve-production ratio’. The Energy Journal (April)

Clarke, Duncan (2007). The Battle for Barrels: Peak Oil and World Oil Futures.

London: Profile Books.

Nasar, Sylvia (1997). A Beautiful Mind. New York: Simon and Schuster

Stern, Roger (2006). ‘The Iranian petroleum crisis and United States national

security. Proceedings of the National Academy of Sciences.

Urban, Julie A. (2006). ‘New age natural gas pricing’. Journal of Energy and

Devopment. Volume 31(1).

Yamaguchi, Nancy (2007). ‘Middle East petroleum sector growing in all directions.

Petromin (March).

Von Neuman, John and Oscar Morgenstern (1944). Theory of Games and Economic

Behavior. Princeton, New Jersey: Princeton University Press.

Pubblicato su www.AmbienteDiritto.it

il 10/06/2007